| SENECA COLLEGE, TORONTO | |

| As Taught by Prof. Tim Richardson School of Marketing and e-Business, Faculty of Business | |

| SENECA COLLEGE, TORONTO | |

| As Taught by Prof. Tim Richardson School of Marketing and e-Business, Faculty of Business | |

DETAILED OUTLINE©

Electronic Commerce and Banking (B2B), (B2C)

| "E-technology

has changed the way we all do business; the way we shop, the way we buy

and sell, the way we close transactions. We seem to be reinventingoutselves

continuously"

"... technology has created fundamental changes in the structure of Canadian banks" What

drives the banks?

|

|

Banking Chapter 7

|

Chapter 7

- Electronic Commerce and Banking

p. 183 Changing Dynamics in the Banking Industry Kalakota's 1997 book is a bit dated but the concepts he discusses still apply to understanding a general overview of the situations facing banks in the e-community. Kalakota notes 5 distinct factors contributing to the new environment - for this class, read, in advance, Chapter 7, and be prepared to discuss the main points

http://ilearn.senecac.on.ca/homepage/Tim.Richardson/iec802/iec802chpt8.ppt |

Ford's article is a bit of a rant, but it contains some interesting points Ford's biggest complaint is that it is difficult to do online transfer of money from accounts you have, to other people's accounts, if they are with different banks. About the only way we can do this, is with the traditional written cheque. The banks don't seem to want to make online links between each other. you might be able to view

the original at

|

Chpt 5 "Cyberbanking" page 173

|

Turban's book has 5 pages

devoted to the subject of banking, with part of the discussion devoted

to personal banking (B2C) and a little bit discussing corporate banking

(B2B)

Turban concludes this section by quoting a Boston Consulting Group 1998 study on the future of banking. While this study may be interesting, 1998 is 2 years ago - which is a lifetime on the Net. WTGR found an article on

the Boston Consulting Group site titled

"To develop enduring online

businesses, however, banks need to move fast, invest capital, and experiment

with new ventures, realizing that some may fail. Such an approach is an

enormous cultural and organizational challenge for most bankers, who have

built their careers on minimizing risk and avoiding mistakes. But

they have no choice: the opportunities are too great and the threats from

newcomers too palpable"

"Skepticism

"Growing Consumer Interest Some bankers question whether

a sufficiently large number of consumers really want to bank online. They

note that in many markets, the growth of the number of online accounts

has lagged expectations. But there is ample evidence that droves of consumers

are poised to embrace online banking. In the United States, more than 15

million consumers checked mortgage rates online in 1999. About the same

number searched online for credit card information. And in the United Kingdom,

more than 5 million consumers logged on to the Internet in 1999 to obtain

financial information. This way of gathering financial information is the

first step toward conducting transactions online. Once consumers start

banking online, momentum can build rapidly. In Australia, there were barely

100,000 online banking customers in early 1999. By the

end of the year, there were 650,000."

The BCG article was written

by Stuart Grief, a vice president in the Boston office of The Boston Consulting

Group. Peter Wetenhall is a vice president in the firms Melbourne office.

Bjørn Matre is a vice president in BCGs Oslo office.

|

|

| Banks

Profits in Canada |

Tom Hirschmann wrote an article

in The Financial Post this summer (02 June 2000) titled

Hirschmann's short article is useful in pointing out that in some cases (Scotiabank and CIBC) part of the massive profits these banks make is either from activities outside Canada, or from other types of activities such as selling real-estate. CIBC for instance made $128 million after-tax gains from the sale of seven real estate properties. |

.

|

www.cba.ca www.cba.ca |

| Industry associations are

one of the best sources of information about an industry as a whole. Often

these associations produce discussion papers and PR material to explain

to government and the public, the opinions and business positions of their

members.

WTGR |

at

www.cba.ca/eng/Consumer_ Kiosk/kiosk_ecomm.htm you will find several links on the CBA web site to pieces of information. Some of these are "backgrounders" which associations use to explain particular issues to the public and government, some of the other pieces are written about e-commerce in general for the audiences that might be people wanting to know the CBA's position in the industry. |

| .

. . |

. |

| This article deals with

the generalities of "buying and selling on the Net", and includes some

bar chart images from the accounting firms. Most of the article is about

how important e-commerce is and how fast it is growing and all the different

things we can do with e-commerce.

WTGR The article is what we call

a "catch all" covering things from the perspective of the business owner,

as well as the customer. They even have a point form list of

|

www.cba.ca/eng/Tools/Brochures/

tools_ecommerce3.htm  |

| This section

is called by the CBA

"Glossary of Terms" but as you will find, it is written for a very "junior" audience, meaning people who have only a introductory understanding of the Net. The fact that the list contains such simple terms illustrates that the CBA thinks most of the people using this portion of the web site are almost complete "newbies" to the web WTGR |

www.cba.ca/eng/Tools/Brochures/

tools_ecommerce_appendice2.htm |

| This section is titled

"Consumer and Business Issues" Not surprisingly, the CBA ranks security and privacy concerns at the top. The way this section is written is to convince the reader that although this is a concern, it is being dealt with and you should feel confidence in going online and buying lots of products with your credit card which will help make the banks and their credit card processing agents even richer! (they also quote extensively from the Angus Reid Group) WTGR |

www.cba.ca/eng/Tools/

Brochures/tools_ecommerce4.htm |

| One thing associations do

often is hold events for members and non-members. Some of these events

are educational oriented, such as seminars.

There is one event in Toronto, contact is Gwen Bailey, Scarborough Chamber of Commerce ph: 416-439-4140 ext. 223 gbailey@scarboroughchamber.com Since so many of these events are TBA and registration is relatively low, maybe the CBA might be interested in assistance from some e-commerce students! |

www.cba.ca/eng/Events/

events_ecommerceseminars.htm |

| Online Banking Report's TrendWatch is a bi-monthly news brief describing the latest trends in the online banking industry. | |

| The Online Banking Report's

TrendWatch Archives section has short paragraphs which cover may hot topics

in online banking.

www.onlinebankingreport.com/home/ trendwatch-archives.html |

Unfortunately this is one of those web sites where the model is "user pay" - to subscribe it costs $700 USD a year - but there is a variety of material that is free in summaries and overviews |

| Our 2000 matrix describing E-commerce and the Canadian banks services to business | Our 2000 matrix describing E-commerce and the Canadian banks services to individuals |

| www.witiger.com/ecommerce/banks~b2b.htm | www.witiger.com/eocommerce/banks~b2c.htm |

| Class

7 |

Banking Alliances

|

The Canadian

banks have had many challenges dealing with the new demands of e-business.

Part

of the problem is that these demands require solutions which are not core

strengths of the banks.

The banks have dealt with this inadequacy in two ways 1. creating new departments in their subsidiary companies to address the new e-business needs 2. buy, merge with, ally with other companies who have existing (or newly existing) capabilities which the new e-business is using WTGR In this section we will look at some of the alliances that have developed and also read about some of the acquisitions the banks made to add more capability. |

| Class

7 |

Banking

Alliances

|

Three Major

Banks plan e-mail payments

The three banks said in a statement in early 2001 that they have signed a letter of intent with CertaPay to offer its ecure e-mail payment option to their customers. Is this alliance a good thing? IDC Canada was quoted as saying that they predict almost a million Canadians will e-mail $2.2 billion in payments in the first 12 months that this option will be availableWhat will the customers do? To make a payment, customers will access their accounts online and give the name and email address of the person receiving the payment. That person will get an e-mail notice explaning how they can securely collect their money. |

.

| Class

7 |

Banking

Alliances

|

Three Major

Banks plan e-mail payments - CIBC, Scotiabank, TD

Certapay's model is to provide service to customers that want to make a payment to someone through an email address. Certapay's involvement with

CIBC, Scotiabank and TD is noted on their web site in Certapay's Feb 2001

press release. In their words:

"CertaPay will enable banks to integrate a P2P payment capability into their existing online services. To make a payment, bank customers will access their accounts online and specify the recipient's name and e-mail address. The recipient will receive an e-mail notification instantly with directions on how to collect the payment securely and in real-time."Does this Canadian system have any advantage over what is being done elsewhere in the world? "CertaPay's service offers the best way to offer P2P payments because it works within the banks' existing secure infrastructure. Most U.S. e-mail payment services operate outside the banking system so consumers need extra accounts, passwords and IDs to send and receive money." |

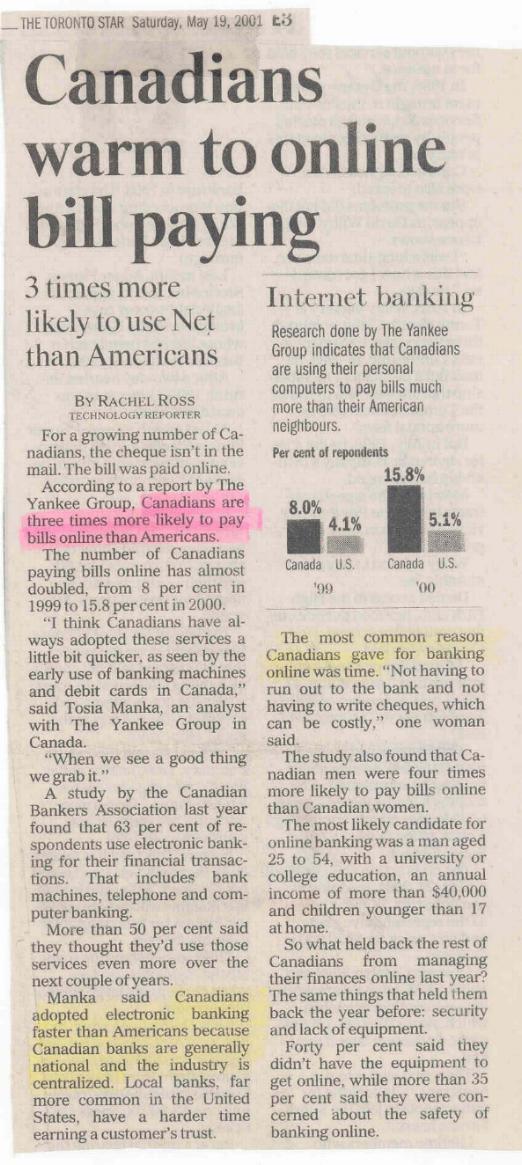

| Online

Bill Paying |

"Canadians

warm to Online Bill Paying"

|

| Class

7 |

Banking

Networking |

Networking: One thing you should do in

collecting contact names for networking, is look at the people listed at

the bottom of press releases. Sometimes when the press release involves

multiple companies the release will give you the name of the communications

people in each company, as well as the name of the executive(s) under which

the effected department(s) operates.

|